2026 for women’s esports is not another wave of motivational stories, but a moment of sober stocktaking. After the rapid growth of 2021–2023, the market entered a phase where survival depends not on who talks louder about inclusion, but on who can build a stable financial framework: media rights, sponsorship packages, digital goods sales, a predictive content plan, transparent KPIs, and spending discipline. Based on the results of 2025—the last full year that logically serves as a baseline for assessing “as of 2026”—a key structural shift is evident: women’s disciplines are moving from a model of “many small tournaments” to a model of “fewer, but more expensive, more media-focused, and more commercially predictable” events. (escharts.com)

Hard metrics set the tone. In 2025, total watch time for women’s tournaments decreased by 7.9%, but the main driver of the decline was not a “loss of interest,” but a reduction in the number of events: there were 52% fewer than in 2024 (after a drop of about 20% the year before). At the same time, average concurrent viewership increased. This is a classic signal of consolidation: small tournaments are disappearing, and attention is concentrating around a few large “anchor” events with better production quality and more clearly defined commercial models. (escharts.com)

An important macro context: the overall gaming market continues to grow (Newzoo/Reuters projected $188.9 billion in global gaming revenues in 2025), but this does not guarantee growth in esports budgets, which depend on measurable ROI. (Reuters) This is precisely why, in women’s esports, the first activities to be cut are those that cannot prove commercial effectiveness.

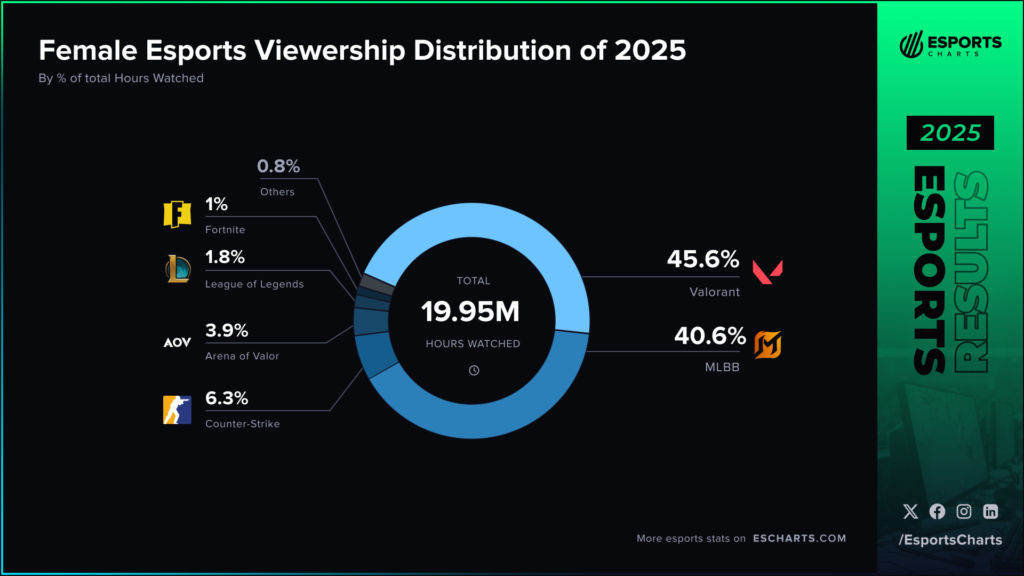

1) The market is no longer multi-game: Valorant and MLBB account for over 90% of views

The least comfortable fact of 2026: women’s esports is now effectively bicentric. Valorant and Mobile Legends: Bang Bang generate over 90% of the viewership of women’s disciplines. (escharts.com)

This is not about genre and not about a “female audience.” It is about institutions and money. These two ecosystems, specifically, have:

- an officially publisher-supported framework (regulations, qualifiers, content discipline, work with partners);

- a marketing “machine” (player heroization, centralized production, regular presence on social media);

- a clear growth path from amateur level to the main stage that can be explained to a player and a sponsor with a single diagram.

In most other disciplines, women’s activities depend on third-party operators or grants—and therefore are the first to be cut during the broader “esports winter.”

2) “Esports winter” hits women’s scenes first: CS2 as a case of the economic limit

The difference between a “publisher ecosystem” and a “tournament operator ecosystem” is most clearly visible in Counter-Strike 2. In October 2025, ESL announced that it was suspending ESL Impact after Season 8, explicitly citing the reason: the current economic model is not sustainable even despite significant investment. (pro.eslgaming.com)

At the same time, media outlets documented the broader context—prior cuts to activities and the withdrawal of organizations, which reduces the scene’s liquidity. (PC Gamer)

For women’s esports, this is not a “failure” but a litmus test: if a discipline lacks a direct monetization engine from the publisher (digital bundles/skins, revenue share, systemic sales), league support becomes dependent on sponsors and “brand-safe” budgets. And those budgets were shrinking across the industry in 2024–2025, forcing even top ecosystems to look for new revenue sources.

A symptomatic example: in 2025, Riot opened its LoL/Valorant leagues in a number of regions to sports betting sponsorships, citing the need to diversify revenues and maintain the long-term viability of leagues amid rising costs and competition for sponsorship budgets. (The Verge)

For women’s products, this creates a double problem: they compete for the same budgets with smaller audiences, and some sponsor categories are additionally constrained by demographics and brand-safety considerations.

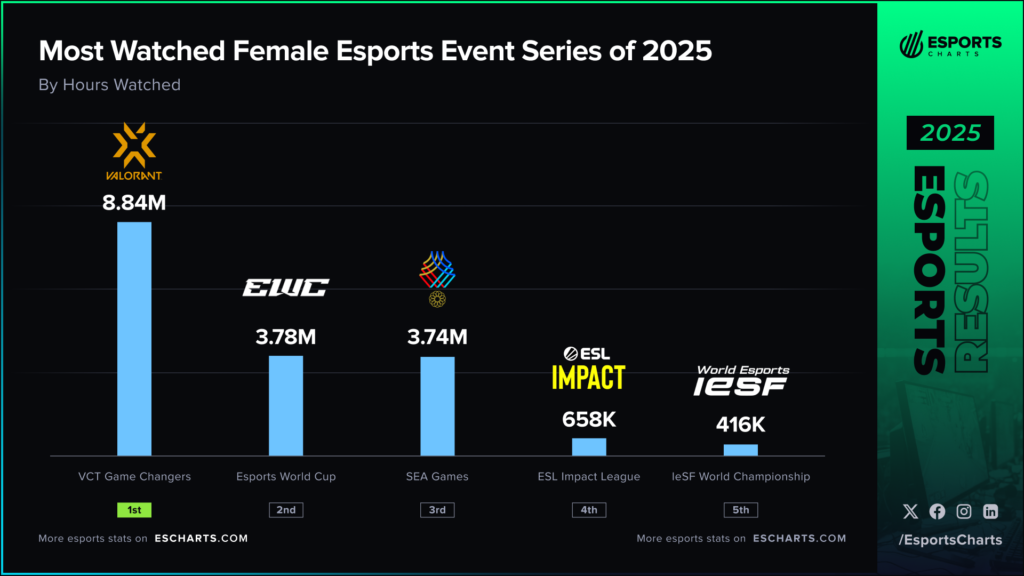

3) Where the current peak in viewership and prize pools is: MLBB Women’s Invitational as the benchmark of a “major event”

In 2025, the biggest peak in women’s esports was recorded at the MLBB Women’s Invitational 2025 (Esports World Cup): the match between Team Vitality Female and Gaimin Gladiators drew 496,954 Peak Viewers, setting a series record and becoming one of the highest peaks in women’s esports overall; Esports Insider emphasized that this peak was achieved with a relatively compact broadcast—around 34 hours of airtime. (escharts.com)

In the “long” metric, this was also an anchor event: the tournament generated 3.78 million Hours Watched. (escharts.com)

The scale of the product was reinforced by its structure: 16 teams and a $500,000 prize pool; the organizer also disclosed the prize distribution for the champion ($150,000) and MVP bonuses. (Liquipedia)

The key detail is not only the numbers, but “how it is done.” MWI is integrated into a large multi-discipline festival that sells partners a package of reach and reputational value. In this setup, the women’s tournament stops being an “add-on” and becomes a content unit that strengthens the positioning of the entire event. This is also where a geographic shift in investment is visible: in 2025, the MENA region accounted for about 20% of the total women’s esports prize pool (approximately $3.3 million for the year). (escharts.com)

Additionally, tournaments of this scale build a pipeline: Xinhua noted that MWI 2025 expanded to 16 teams and featured qualifiers in 57 regions. (english.news.cn)

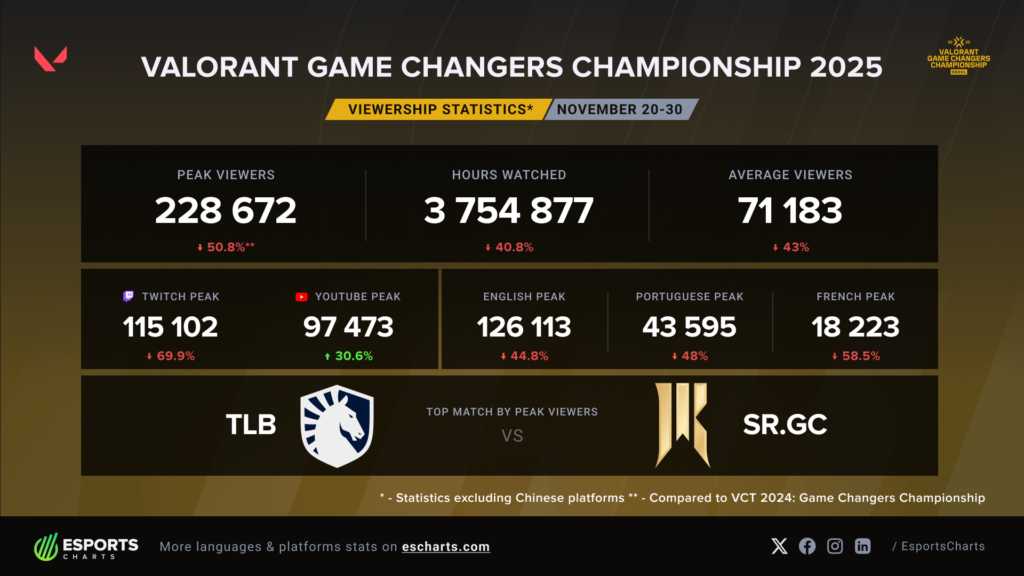

4) Valorant: declining peaks, but the strongest “media value” economy

On the surface, 2025 looks like a rollback for Game Changers. The peak of the Valorant Game Changers Championship 2025 grand final reached 228.7k viewers—more than 50% lower than the 2024 record. (escharts.com)

However, in 2026 the value of GC is increasingly measured not only by peak viewership, but by Media Value—an estimate of advertising equivalency for brands. According to Esports Charts, GC Championship 2025 generated $1.88 million in Media Value—the highest figure among all women’s tournaments that year. (escharts.com)

The event also has a “mature” competitive framework: 10 teams and a $500,000 prize pool. (Liquipedia)

Why does this matter? Because Valorant is not selling “the mere fact of a women’s tournament,” but a packaged media product with clearly defined partner slots, serialized storytelling, a consistent content rhythm, and active co-streaming. Here again, the publisher’s advantage as the ecosystem’s “central bank” is evident: Riot reported that in 2024 it distributed $78.4 million to teams across the VCT ecosystem under a revenue-share model, with $44.3 million coming from digital item sales alone. (valorantesports.com)

For scale: the main Valorant Champions 2025, according to Esports Insider, recorded a 1.47 million peak and 47.58 million hours watched—the order-of-magnitude difference explains why GC exists not as an “alternative to Champions,” but as a separate vertical product optimized for partner KPIs. (Esports Insider)

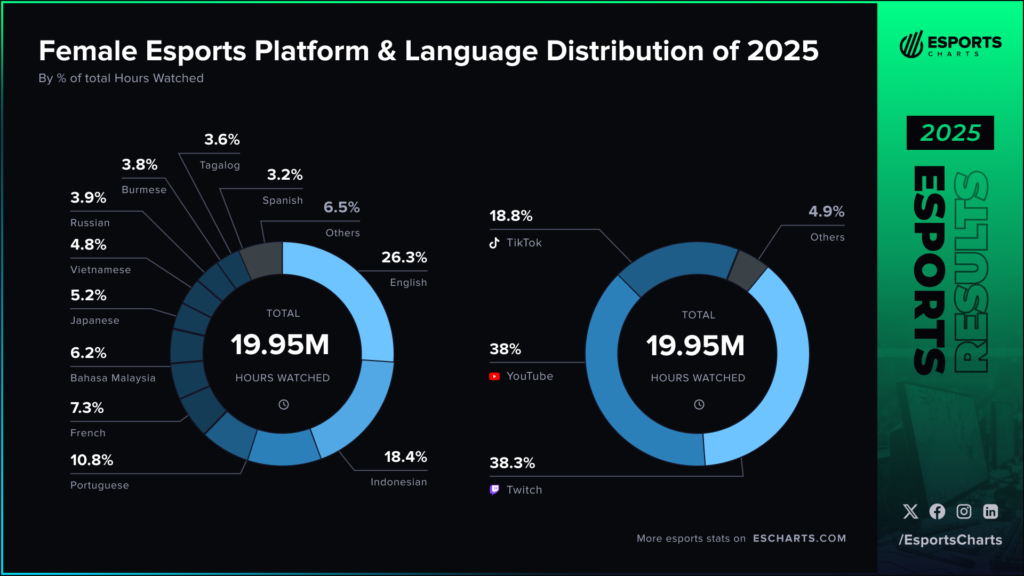

5) Platforms and distribution: YouTube and TikTok are reshaping the fan funnel

One of the most practical trends is the shift in media platforms. According to Esports Charts, in 2025 YouTube’s share in women’s broadcasts increased by approximately 10 percentage points, while TikTok’s share grew by 7.5 p.p.; at the same time, Twitch and YouTube reached approximate parity. (escharts.com)

In product terms, this means:

- TikTok functions as the top of the funnel (algorithmic reach, short clips, rapid acquisition of new viewers);

- YouTube acts as a “television” channel for major finals and as an archive that strengthens the long tail of views;

- Twitch serves as a platform of “habit” and regularity that retains the core audience.

For women’s disciplines, where not only the number of fans is critical but also conversion into loyalty and monetization, such a distribution reinforces the model of “fewer tournaments, but larger and more expensive ones.”

Consolidation raises the bar: when there are fewer events, each one becomes more costly both as an opportunity and as a risk. Clubs need athlete marketing, content, and measurable sponsor deliverables; players need media discipline, not just competitive form.

6) The prize-money ceiling for female players remains low — and this is a structural constraint

Even without touching on salaries and private contracts, prize money illustrates the scale of the imbalance. According to the EsportsEarnings database, the top earnings among women by career prize money are led by Sasha “Scarlett” Hostyn — $472,111. (Esports Earnings)

By contrast, in some men’s disciplines the top of prize winnings is measured in millions; for example, in Dota 2 the leaders of the rankings have more than $7 million in career prize money. (Межа)

This matters as a factor of professionalization: when prize money is low, a career becomes dependent on salaries and sponsorships; when there are no salaries — on survival. That is why the emergence of regular $500k events (MWI, GC Championship) is critical — they raise the “ceiling,” create an argument for clubs, and set a market reference point that can be replicated. (Liquipedia)

7) Toxicity of the environment is not “ethics,” but the economics of entry

In 2026, another topic shifts from morality to finance: the safety of the environment as a factor of talent conversion. Polygon, referring to an analysis of voice communications in Valorant, cited figures that should be read as a “cost of entry”: the sample recorded very high shares of profanity (80.8% of messages contained swearing) and a measurable share of sexual harassment (14.17%). (Polygon)

For organizations, this means costs: moderation, psychological support, communication protocols, and work with reputational risks. That is why “separate circuits” (Game Changers, Impact, etc.) perform not only a symbolic function, but the role of risk-reduction infrastructure: they increase the chance that a female player will remain in the system long enough to turn potential into results.

8) Which KPIs realistically measure progress in 2026

To avoid the amateurish notion of “there is more visibility,” progress in women’s esports should be measured by three groups of KPIs that correlate with sustainability:

- Professionalization: the number of rosters with stable compensation (salary, coaching staff, management) and the length of contract horizons.

- Integration: the number of cases where women’s rosters or players enter open mixed tournaments and do not appear statistically random.

- Content monetization: media value, the structure of sponsorship packages, digital goods sales, the share of co-streams, and platform retention.

A demonstrative example of integration logic is Imperial Valkyries: participation and public matches against NAVI became one of the most media-liquid stories of the year; in 2025, 2.32 million Hours Watched were recorded around this storyline. (escharts.com)

Such cases are important not as a “sensation,” but as proof that women’s esports can produce content consumed by a broader audience, not only the internal community.

The conclusion for the first part is simple: as of 2026, women’s esports is a market going through the same cycles as mainstream esports—event contraction, concentration in a few tentpole formats, high dependence on publisher economics and the sponsorship climate. The strongest segments are where three things coincide: official support, a large-scale media product, and a clear financial framework. The most vulnerable are where the scene lacks its own monetization engine and is forced to exist as a cost item rather than as a business unit with its own P&L. This is the main